Vestbee, Europe’s leading platform for startups, VCs, accelerators, and corporates, has just released its VC funding in CEE report — Q1 2025, revealing a mixed quarter for the region. The report highlights a region increasingly aligned with global AI trends, but struggling with structural headwinds: declining deal flow, retreating foreign capital, and limited local fund capacity.

CEE capital follows the AI wave with ElevenLabs emerging as an outlier

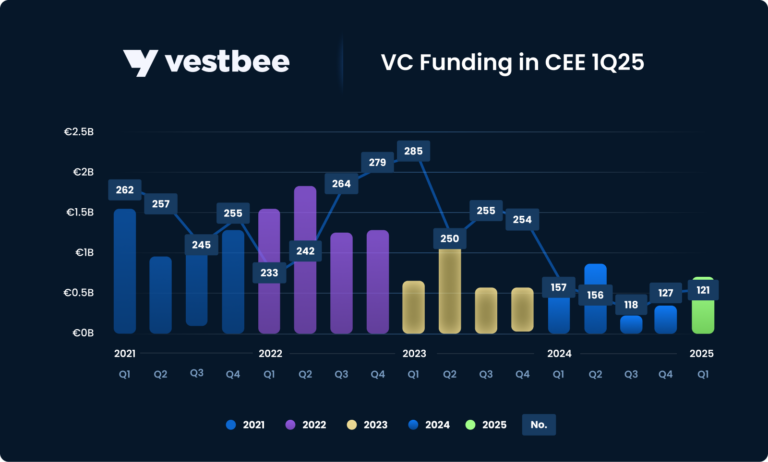

In Q1 2025, venture capital investment in Central and Eastern Europe (CEE) reached €700 million, marking a 9% year-over-year increase. However, this figure was significantly inflated by a single landmark transaction — the €170 million Series C round raised by Polish-founded AI voice startup ElevenLabs. When adjusted for this outlier, total funding declined to €530 million, revealing a 17% decrease compared to Q1 2024.

This divergence reflects the broader global pattern of a growing polarization within the venture landscape. Those late-stage AI startups with clear market traction continue to raise large rounds, whilst younger companies are increasingly facing tighter capital constraints and longer fundraising cycles.

Mirroring the capital concentration, deal activity across the region also contracted, with the number of rounds falling from 157 in Q1 2024 to 121 in Q1 2025, a 23% year-over-year decline. The largest disclosed rounds this quarter included ElevenLabs (€170M), Mews (€66M), and Blackwall (€45M) — each reflecting a trend where VC capital tends to cluster around a few breakout companies with proven traction in AI and SaaS.

“To unlock the next phase of growth, the CEE region must address both structural and cyclical challenges that are widening its funding gap,” commented Ewa Chronowska, CEO at Vestbee. “While global investors are increasingly drawn to mature markets with immediate scalability, CEE’s startups are left navigating capital scarcity, limited local fund capacity, and an underdeveloped exit landscape. Without renewed investor confidence, stronger domestic funding mechanisms, and clearer pathways to liquidity, the region risks stalling its innovation momentum just as its strategic relevance is rising.”

Nevertheless, the region’s long-term potential is becoming more evident. The combined enterprise value of CEE startups reached €243 billion, a 35% increase from €180 billion in 2020, reflecting growing market maturity and the ecosystem’s evolving capacity to generate scale and value.

Sectoral trends and regional leaders

Poland led the region by deal count (36 rounds), followed by Estonia (18) and Czechia (17). The most active local VC funds included, among others, J&T Ventures, Interactive Venture Partners, SMOK VC, Day One Capital, Inovo VC, Tera Ventures, Radix Ventures, Underline Ventures, bValue Fund, and Impact Ventures. Moreover, the significant presence of global investors such as Tiger Global Management, Battery Ventures, Kinnevik, and Goldman Sachs Alternatives, in landmark deals such as Mews showed the selective but strategic interest from international capital sources.

Sectoral interest in CEE aligned closely with global priorities, with AI, healthtech, biotech, financial services, and SaaS emerging as the most actively funded verticals.

Europe keeps pace while global VC follows AI and big deals

Global venture funding rebounded sharply in Q1 2025, reaching $113 billion — its strongest quarter since mid-2022. Yet this apparent resurgence was mostly driven by a single outlier — OpenAI’s record-breaking $40 billion round, which alone accounted for more than one-third of global capital deployed. Excluding this deal, global investment levels were effectively flat year-over-year and down quarter-over-quarter, reflecting a more subdued funding landscape.

The quarter reinforced a broader shift toward late-stage and AI-focused investments, with over half of global VC capital flowing into AI-related ventures. Meanwhile, early-stage and seed financing continued to decline, highlighting a growing polarisation in the venture capital landscape.

In Europe, venture activity held firm at $12.6 billion, marking a period of relative stability after the volatility of post-pandemic years. However, Europe’s share of global venture capital fell to 11%. Health and life sciences led the continent’s financing rounds, attracting approximately $4 billion, or one-third, of all European VC funding, with AI and biotech as the remaining top-performing sectors. Yet, momentum was increasingly concentrated in the mature ecosystems — primarily the UK and Germany, with smaller and emerging markets struggling to capture consistent deal flow.

Dig deeper with Vestbee’s full report

For a deeper dive into the trends shaping CEE’s venture capital landscape, including detailed analysis and data on sectoral performance and regional investment, access Vestbee’s full VC funding in CEE report — Q1 2025.

source: Vestbee

{kind=link}

{kind=link}

{kind=link}

{kind=link}